|

|

发表于 14-2-2007 12:24 AM

|

显示全部楼层

发表于 14-2-2007 12:24 AM

|

显示全部楼层

怎么翻出这么久的贴? |

|

|

|

|

|

|

|

|

|

|

|

发表于 21-2-2007 03:19 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 22-3-2007 03:02 PM

|

显示全部楼层

wow,supermx 掉到2。27 LIAO。。。。。

可以买吗?

好股来的。。。。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 22-3-2007 03:18 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 22-3-2007 03:18 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 22-3-2007 03:18 PM

|

显示全部楼层

回复 #80 tmm123 的帖子

|

是因為split的關係才會出現2.27, split之前是4.54 |

|

|

|

|

|

|

|

|

|

|

|

发表于 22-3-2007 03:22 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 28-7-2007 07:42 PM

|

显示全部楼层

|

好久没人回帖了,最进的事业做很大了,大家对于他,各位给点意见吧 |

|

|

|

|

|

|

|

|

|

|

|

发表于 28-7-2007 07:51 PM

|

显示全部楼层

等待时机而已

和KLCI的本益比比起来还是undervalue的 |

|

|

|

|

|

|

|

|

|

|

|

发表于 28-7-2007 08:16 PM

|

显示全部楼层

|

估值是2。50,现在比估价还要低了,还记得拆细下来是2。27,我还在等待加码 |

|

|

|

|

|

|

|

|

|

|

|

发表于 27-8-2007 11:52 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 29-8-2007 05:49 PM

|

显示全部楼层

|

每股盈利低了,配股收购的原因,业绩与上一季不相上下,还可以接受,但市场上还有很多更好的选择 |

|

|

|

|

|

|

|

|

|

|

|

发表于 1-11-2007 09:43 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 1-11-2007 09:50 PM

|

显示全部楼层

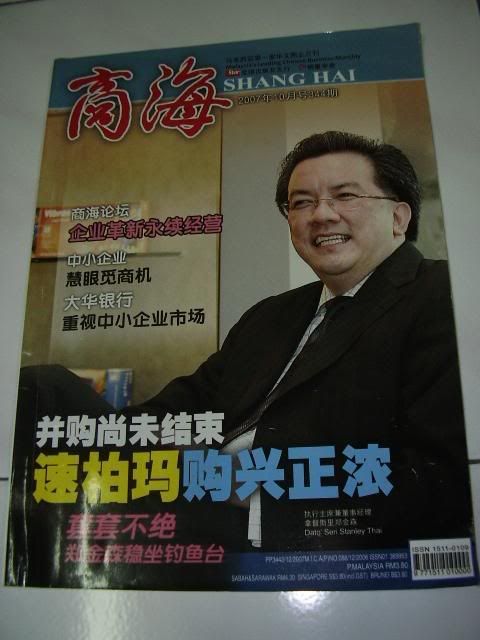

从pya_ch兄的<三国鼎立?>摘录一些精彩帖子。

原帖由 pya_ch 于 5-10-2007 06:48 PM 发表

三国鼎立?

今天看了商海的一篇文章,

其中作者提到大马手套业的情况,

他说,顶级以量取胜,利用产量优势大打价格战,

高产则是历史悠久根深蒂固,

速柏玛则是超级马,虽然数量不及对手,

不过在品牌创造和高档市场很吃得开,

其中又以速柏玛最是积极,

通过收购亚太来强攻底成本市场,

自己则以超然地位持续扩张,

对手套业有研究的各位又怎么看手套业的相互竞争呢?

你们觉得最终谁会脱颖而出呢?

原帖由 pya_ch 于 5-10-2007 07:12 PM 发表

作者用一个寓言故事来比喻,

龟兔赛跑的故事大家都知道了,

可是随着时代的变迁,

有了新的演变,

即第二次的龟兔赛跑,

这次乌龟利用了自己的长处,

巧妙的击败了来势汹汹的兔子,

然而作者有着我没听过的第三次,

他说这次的赛跑有了圆满的结局,

即兔子背着乌龟走旱路,

而乌龟则背兔子渡过了那条河,

双双以更短的时间到达终点,

达到了双赢的局面,

可是这虽然完美,

却很难出现在现实中,

倒是他引用可口可乐的例子倒比较可行,

其实他们目前大可以不必争的你死我活,

我们马来西亚目前"只"占有了世界手套55%的市场,

要争也争那剩下的45%啊,

可口可乐就是因为这样,

所以才摆脱了百事的纠缠,

走到今天的地位,

所以林董事长,

这期的商海你看了没有

希望你暂时将心思放在那45%的市场,

按自己的脚步前进,

千万不要这么快就和supermax打肉搏战,

在自己的市场没有达到绝对的领先优势时,

不要这么快就去挑战supermax的高档市场啊,

小心两头不到岸,我的致富梦有四份一看你了

原帖由 pya_ch 于 15-10-2007 01:47 PM 发表

基于市场更加看好supermax给予topglov的威胁更大,

所以我就暂时偷个懒,

集中比较这两家公司就好,

这里的资料当然不够齐全,

但是已经是我手上拿得出来的数据了,

年份 营业额(000) 净利(000) 股东回酬率(%)

topglov supermax topglov supermax topglov supermax

2001 138,862 17,217 14,680 4,222 16.11 6.31

2002 180,202 84,604 16,102 8,585 15.63 12.09

2003 265,089 141,162 23,349 17,380 19.11 15.56

2004 418,133 218,423 38,932 30,210 26.25 21.69

2005 641,827 284,688 53,447 36,273 27.61 17.74

2006 992,511 400,324 78,392 39,749 29.92 16.57

2007 619,652 245,041 50,476 28,323 9.64 10.49

*2007为半年业绩

虽然supermax的业绩成长惊人,

然而topglov也并没有松懈下来,

以roe而言,07年是暂时以supermax为更好,

过往则以topglov遥遥领先,

究竟谁才是真霸主,

也许要等多几年才能评断吧,

但是无可否认的是,

它们的努力,为我们这些小股东创造了投资致富的机会,

在这里仅献上我的由衷感谢,

是他们的努力不懈,

为在这只为自身利益着想的国家里,

给了我们希望,

原来愿意为股东创造财富的还是大有人在,

原来当马来西亚的其它民族以及大部分的华商,

将道义放两旁,利字摆中间的时候,

还是有少许人将中华五千年美好的品德传乘下来了,

独乐乐不如众乐乐,

所以当初klse.8k,os,harimau等众前辈才会不辞劳苦的分享,

将自己辛苦的研究以及功课公布,

希望能为大家提供一个学习的地方,

一个交流的地方,一个互相交换意见的地方,

所以请大家多提意见,少点人身攻击

(尤其之前投资于大马某家电讯公司的小股东,

当他们知道某些消息后,应该会跟我一样这么庆幸吧)

原帖由 chengyk 于 22-10-2007 12:08 PM 发表

supermax 和 topglove 都能保持一定的增长率。。。其实,两个管理层都很好。在控制成本方面做得很出色,就连橡胶的价格偏高,也影

响不到他们。。。

我觉得林博士野心比较大,他有称霸世界的 野心,而且他做到。相比,陈先生就比较逊色,从他的年报里,我看

不出他有爬过topglove 得野心。。。

原帖由 pya_ch 于 22-10-2007 12:57 PM 发表

可是商海的专题作者就说了,

当初他访问的时候,

郑老板在回答他的问题的时候说到,

他的目标是要将supermax带到世界之巅,

成为最大的手套厂,

只怕他是拌猪吃老虎

以本益比而言,supermax是占优的,

以07年的数据而言,

supermax仍是占优的

[ 本帖最后由 Mr.Business 于 1-11-2007 09:51 PM 编辑 ] |

|

|

|

|

|

|

|

|

|

|

|

发表于 1-11-2007 09:53 PM

|

显示全部楼层

原帖由 Mr.Business 于 26-10-2007 07:37 PM 发表

再讲讲商海这一篇文章,文章作者很赞赏Supermax收购APLI和Seal Polymer的举动。可是如果我们回顾历史的话,其实我们可以发觉Supermax的这两项收购并不是非常顺利的。

首先,Supermax是没有经过精密调查就收购这两间公司的股份,接收公司的管理权才发现很多的问题。

1. APLI季季亏损,直到最近两个季度才开始小赚;

2. APLI的越南工厂的boiler出了问题,机器要再次整修,最近工厂才重新运作;

3. Seal Polymer的audited result和unaudited result出现很大的差别。

收购公司并不是想象中那么容易。。。

原帖由 pya_ch 于 26-10-2007 11:15 PM 发表

其实创业不难,只要胆大财粗就可以了

但是守业就不同了,

你不进就退,而且身为上市公司,

如果不思进取,小股东也不肯啊,

所以扩充是不能避免的,

但是扩充也不是一帆风顺的,

看看supermax的并购,

看看topglov在中国的扩展计划,

有时我觉得我们身为小投资者是幸福的,

只要出钱,然后留意一下公司的经营情况,

只要一不对头,钱撤了就跑

但是也有板有不幸的(如金鹏 ) )

投资的黄金守则,1.不要亏钱2.不要忘了第一条

要不亏钱说难不难,

如果只是纯粹的想资本增值,

那就容易,想输都难,只要投资众所周知的好公司就行,

但是如果想挑战自己,

寻找那种胜利的快感,

那就很多东西好学咯

那个时候记得,房里别忘了贴这黄金守则啊

原帖由 piao2 于 28-10-2007 06:58 PM 发表

生意兄说言即是。

看回我老板一年多前入股(成为major shareholder)的公司,起初以为该公司的产品可以补助我方的range,可是接二连三的问题不断浮现,直到最近又有一位股东离开,我才领悟到这个硬道理。

之前,有位和该公司老板相熟的供应商曾经好意表达,要注意此人的言行,我也不以为意的转达于老板。想起这段事,不知我老板会不会说:早知如此。。。。

呵呵,做生意不熟不做,就算熟悉,品德才是更重要的考量点呀!

做生意从小做大是一门学问,而收购又是另一门学问了。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 1-11-2007 09:58 PM

|

显示全部楼层

不幸给小弟言中,Supermax属下的APLI又出事了!!!

连接。

General Announcement

Reference No CCS-071031-3783B

Company Name : APL INDUSTRIES BERHAD

Stock Name : APLI

Date Announced : 31/10/2007

Type : Announcement

Subject : APLI INDUSTRIES BERHAD (“APLI” OR “THE COMPANY”))

- Net Profit Variance in Audited and Unaudited Accounts

Executive Summary :

-

Contents :

Net Profit Variance in Audited and Unaudited Accounts

Based on the audited financial statements of APLI Group for the financial year ended 30 June 2007, the Net Loss After Tax amounting to RM 21.1 million, which is higher than the unaudited result (i.e. RM 4.5 million) for the same period. Details are as follows:

| Unaudited | Audited | Variance | | | | RM’000 | RM’000 | RM’000 | | | | Loss before taxation | (3,451) | (17,571) | (14,120) | | | | Taxation | (1,068) | (3,520) | (2,452) | | | | Loss after taxation | (4,519) | (21,091) | (16,572) | | |

The difference arose from the audit adjustments made, mainly attributed to the following:

1. Accounting treatment for land lease rental fees payable in respect of the unoccupied plot.

The Company had purchased a large plot of land for its Vietnam plant but large portion of the total land area is currently unoccupied. In this respect, the land lease rental fees payable was charged off based on the occupied land area while the remaining plot was capitalised as “pre-operating expenses”, amounting to USD 111,660 (RM 385,227).

However, according to the Vietnamese accounting standards, such item should instead be expensed off regardless of whether the land area has been occupied or not. Therefore, an additional amount of USD 111,660 (RM 385,227) has to be charged out as expenses (land lease rental). Total land lease rental charged out for FY06/07 is now RM 854,427 instead of RM 469,200.

2. Classification of certain machineries and equipment installed at Vietnam plant resulting in depreciation not charged.

Machineries and equipment purchased by the company’s Vietnam plant were not reclassified from “Construction in Progress” to “Fixed Assets” since they were commissioned. These items, once classified as “Fixed Assets” will be subject to annual depreciation charge. The Auditors had highlighted that the depreciation charge for these items was not recognised for 2 financial years. Therefore, an additional depreciation charge of USD 233,067 (RM 804,080) will be charged out during the audit year.

3. Damaged machinery parts not written-off.

The Company’s Vietnam plant is housing a number of damaged formers (being part of the machinery). Previously, it was anticipated that these formers could be disposed off as scrap and thus there was no decision to write-off.

However, the Auditors are of the opinion that these formers are not in recyclable condition and could not be easily disposed of. As such, these formers had to be written-off amounting to USD 143,474 (RM 494,985).

4. Computation of deferred tax asset and deferred tax liability.

(a) Based on the profits reported in Asia Pacific Latex Sdn Bhd’s unaudited financial results, a deferred tax asset was recognised amounting to RM 275,400. However, the audited financial statements revealed that the company recorded losses instead of profits as per unaudited results and thus such deferred tax asset has to be reversed accordingly.

(b) The Auditors’ computation of the deferred tax liability differs from the Management’s computation. Such difference resulted in under provision of deferred tax liabilities amounting to RM 343,266.

5. Accounting treatment on settlement of corporate tax underpaid.

IRB had carried out a tax investigation on APL Products Sdn Bhd’s tax affairs, for the year assessment 2001 to 2004. The outcome of the investigation revealed that the total tax underpaid amounted to RM 2,470,000 (including the tax penalty). Under initial understanding, this amount was supposed to be settled against the tax benefit carried forward from prior years and thus only need to be adjusted against deferred tax asset (i.e. 27% of the underpaid tax which is equivalent to RM 666,900).

However, the Auditors highlighted that the above item should instead be fully adjusted against the company’s tax credit. Therefore, additional tax expense should be recognised amounting to RM 1,803,100, making the total of RM2,470,000 for the entire FY06/07.

6. Downward revaluation of finished goods

All finished goods held are valued based on actual product costing.

However, the Auditors viewed certain finished goods as slow-moving stocks and thus they should be valued lower. This had resulted in a downward revaluation of such goods by RM 1,691,000.

7. Billing of finished goods sent to specific plant of an affiliated company for QC and packing and onward shipment to external customers.

During the financial year, there were certain goods transported from a manufacturing plant of APLI to another plant of an affiliated company for the purpose of QC and packing. These goods were then directly shipped to the external customers. The trading arm then issued sales invoices to overseas customers.

However, the Auditors highlighted that there were instances of incorrect billing where sales invoices had been erroneously issued based on shipment of goods to the plant handling the specific QC and packing functions.

As the shipment of these goods were already supported by sales invoices issued by the trading arm, the incorrect billing had resulted in sales being double taken-up amounting to RM 7,273,560.

8. Purchases of raw materials not taken up due to timing differences

There were several commercial invoices on purchases of raw materials which were captured as July 2007 transaction instead of June 2007. Although the commercial invoices were dated in July 2007, the delivery of stocks took place in June 2007.

Therefore, the purchases (amounting to RM 3,501,382) should be recognised in June 2007, i.e. at the point when the company took delivery of the stocks.

[ 本帖最后由 Mr.Business 于 1-11-2007 10:16 PM 编辑 ] |

|

|

|

|

|

|

|

|

|

|

|

发表于 1-11-2007 10:10 PM

|

显示全部楼层

连接。

General Announcement

Reference No CC-071031-59831

Company Name : APL INDUSTRIES BERHAD

Stock Name : APLI

Date Announced : 31/10/2007

Type : Announcement

Subject : APLI INDUSTRIES BERHAD (“APLI” OR “THE COMPANY”))

- ANNOUNCEMENT PURSUANT TO THE AMENDED PRACTICE NOTE NO. 17/2005

Executive Summary :-

Contents :

1. INTRODUCTION

Pursuant to the Paragraph 8.14C of the Listing Requirements (“LR”) of Bursa Malaysia Securities Berhad (“Bursa Securities”) and Practice Note No. 17/2005 (“Amended PN17”), the Board of Directors of APLI wishes to announce that, based on the consolidated audited financial statements for the financial year ended 30 June 2007, as announced 31 October 2007, APLI is considered an Affected Listed Issuer as the Company’s shareholders’ equity on consolidated basis amounting to RM46.435 million is less than twenty five percent (25%) of its total issued and paid-up share capital of RM347.612 million of the Company and such shareholders’ equity is less than the minimum issued and paid-up capital as required under Paragraph 8.16A(i) of the LR (“the First Announcement”)

2. OBLIGATIONS OF THE COMPANY AS AN AFFECTED LISTED ISSUER PURSUANT TO PN17

Pursuant to the Amended PN 17, APLI as an Affected Listed Issuer is required to comply with the following:-

(i) submit a plan that is substantive and falls within the ambit of Section 212 of the Capital Market and Services Act 2007 to regularise its financial condition (“Regularisation Plan”) to the Securities Commission and other relevant authorities for approval within eight (8) months from the date of the First Announcement (“Submission Timeframe”);

ii) implement the Regularisation Plan within the timeframe stipulated by the relevant authorities(“Implementation Timeframe”);

iii) announce the status of its Regularisation Plan and the number of months to the end of the relevant timeframes on a monthly basis until further notice from Bursa Securities;

iv) announce its compliance or non-compliance with a particular obligation imposed pursuant to the Amended PN 17 on an immediate basis; and

v) announce the details of the Regularisation Plan (“Requisite Announcement”), which shall include timeline for the complete implementation of the Regularisation Plan. The Requisite Announcement must be made by a merchant banker or a participating organisation that may act as a principal adviser under the Securities Commission’s Policies and Guidelines on Issue/Offer of Securities.

3. CONSEQUENCES OF NON-COMPLIANCE WITH THE OBLIGATION

In the event APLI fails to comply with the obligations to regularise its condition, all its listed securities will be suspended from trading on the fifth (5th) market day after the expiry of the Submission Timeframe or implementation Timeframe, as the case may be, and de-listing procedures shall be taken against the Company.

4. STATUS OF PLAN TO REGULARISE CONDITION

The Board of Directors of APLI is currently looking into formulating the Regularisation Plan to regularise the condition of the Company. Upon completion, the requisite announcement outlining the Regularisation Plan shall be announced to Bursa Securities in due course.

This announcement is dated 31st day of October 2007. |

|

|

|

|

|

|

|

|

|

|

|

发表于 1-11-2007 10:24 PM

|

显示全部楼层

帐目出问题,管理不良,进了PN17。。。APLI的坏消息真是够多了!却不见管理层出来说说话!

希望这不是有心人想要低价收购APLI而出的阴谋!!!不然就太可怕了。。。。

XXXXX

看回以下这旧新闻,讽刺讽刺。。。希望有投资APLI或Supermax的网友可以出来说说你们的看法。

Wednesday November 8, 2006

APLI to be back in the black

By SHILING WOON

SUBANG JAYA: APL Industries Bhd (APLI) expects its upgraded technology for glove making, which will double the production of its Go-Dau plant in Vietnam, to help the group return to the blackin the current fiscal year.

Managing director Datuk Seri Stanley Thai said the Go-Dau plant currently utilised only 50% of its installed capacity to produce 45 million gloves per month due to old equipment constraint.

Datuk Seri Stanley Thai (left) exchanging documents with Ecotherm managing director Yap Mew Sang. Looking on are APLI’s senior management.

The plant is being managed by APL International Inc Ltd (APLI Vietnam).

“We expect the new technology, designed and implemented by Ecotherm SdnBhd, to boost group revenue, as well as expand the plant's output by 92% from 45 million gloves per month,” he said.

Thai was speaking to reporters after an agreement signing between APLI Vietnam and Ecotherm yesterday.

Therefore, he said, the group was confident of doubling its monthly production to 86 million pieces by the third quarter of its fiscal year when Ecotherm's advanced boilers and dipping processes were fully operational.

He added that APLI was confident of seeing a 30% growth in group revenue in the financial year 2007.

For the financial year ended June 30, APLI posted a bigger net loss of RM25.2mil compared with RM23.4mil in the previous year. Revenue was at RM193.7mil, an increase of 8.3% from RM178.9mil recorded earlier.

Thai said the new technology would help the group save at least 30% on its manufacturing costs.

Under the RM8mil contract, Ecotherm was to supply and install two units of the latest technology broilers as well as to upgrade six dipping processes lines.

Ecotherm started the installation and upgrading works last week. Thesix two-tier production lines are expected to be commissioned by June2007.

“We expect APLI's total production capacity, including that of its two Malaysian plants, to be about 5.3 billion gloves per annum by June 2007,” Thai said.

The two local plants have a yearly production capacity of 2.7 billion gloves.

Thai said APLI Vietnam's planned investment of about RM35mil to add six more two-tier production lines in the second half of next year would expand total group production capacity to 7.1 billion gloves by end-2007.

http://thestar.com.my/news/story.asp?file=/2006/11/8/business/15950691&sec=business

[ 本帖最后由 Mr.Business 于 1-11-2007 10:26 PM 编辑 ] |

|

|

|

|

|

|

|

|

|

|

|

发表于 1-11-2007 10:30 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 1-11-2007 10:32 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

| |

本周最热论坛帖子 本周最热论坛帖子

|

1884

1884  72

72