|

|

楼主 |

发表于 1-12-2016 06:27 AM

|

显示全部楼层

EX-date | 06 Dec 2016 | Entitlement date | 08 Dec 2016 | Entitlement time | 05:00 PM | Entitlement subject | Rights Issue | Entitlement description | Renounceable rights issue of 133,333,131 new ordinary shares of RM0.05 each in Bioalpha ("Bioalpha Shares") ("Rights Shares") at an issue price of RM0.20 per Rights Share on the basis of 1 Rights Share for every 5 Bioalpha Shares held as at 5.00 p.m. on 8 December 2016, together with 133,333,131 free new detachable warrants ("Warrants") on the basis of 1 Warrant for every 1 Rights Share subscribed | Period of interest payment | to | Financial Year End | 31 Dec 2015 | Share transfer book & register of members will be | to closed from (both dates inclusive) for the purpose of determining the entitlement | Registrar or Service Provider name, address, telephone no | SYMPHONY SHARE REGISTRARS SDN BHDLevel 6, Symphony HousePusat Dagangan Dana 1Jalan PJU 1A/4647301Petaling JayaTel:0378490777Fax:0378418151 | Payment date |

| | a.Securities transferred into the Depositor's Securities Account before 4:00 pm in respect of transfers | 08 Dec 2016 | b.Securities deposited into the Depositor's Securities Account before 12:30 pm in respect of securities exempted from mandatory deposit |

| | c. Securities bought on the Exchange on a cum entitlement basis according to the Rules of the Exchange. | Number of new shares/securities issued (units) (If applicable) | 133,333,131 | Entitlement indicator | Ratio | Ratio | 1 : 5 | Rights Issue/Offer Price | Malaysian Ringgit (MYR) 0.200 | Par Value | Malaysian Ringgit (MYR) 0.050 |

Despatch date | 13 Dec 2016 | Date for commencement of trading of rights | 09 Dec 2016 | Date for cessation of trading of rights | 19 Dec 2016 | Date for announcement of final subscription result and basis of allotment of excess Rights Securities | 04 Jan 2017 | Listing Date of the Rights Securities | 10 Jan 2017 |

Last date and time for | Date | Time | Sale of provisional allotment of rights | 16 Dec 2016 | | 05:00:00 PM | Transfer of provisional allotment of rights | 21 Dec 2016 | | 04:00:00 PM | Acceptance and payment | 27 Dec 2016 | | 05:00:00 PM | Excess share application and payment | 27 Dec 2016 | | 05:00:00 PM |

|

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 5-1-2017 06:26 AM

|

显示全部楼层

本帖最后由 icy97 于 6-1-2017 06:02 AM 编辑

科鼎附加股凭单超购1.22倍

2017年1月6日

(吉隆坡5日讯)科鼎(BIOHLDG,0179,创业板)旗下的附加股及凭单获得市场的热烈回响,认购率达122.07%,相等于超额认购1.22倍。

根据昨天的文告,该公司接获市场认购1亿6276万685股附加股,但给予认购的份额,仅有1亿3333万3131股,相等于22.1%的超额认购率。

去年9月7日,科鼎建议,以每5股配1股附加股送1凭单比例,发出1亿3333万3333股新股和相同数额的凭单。

根据每股20仙的发售价估算,该批附加股预计可筹得约2670万令吉。

其中,将近一半的金额将在未来18个月,在大马、印尼和中国推出27个新产品。

另外的850万令吉,则会用来拓展农业业务。其余的金额则会当做资本开销、营运资本等。

科鼎董事经理韩丁国通过文告向股东致谢,并对超额认购一事感到高兴。

“所筹获的资金,可让我们继续推动增长,并巩固我们在大马、印尼和中国的据点。”

由于大部分的资金将用来增加产品范围,因此,他乐观看待这可成为巩固增长的催化剂,显著贡献未来18个月的净利。【e南洋】

Type | Announcement | Subject | NEW ISSUE OF SECURITIES (CHAPTER 6 OF LISTING REQUIREMENTS)

FUND RAISING | Description | BIOALPHA HOLDINGS BERHAD ("BIOALPHA" OR "COMPANY")RENOUNCEABLE RIGHTS ISSUE OF 133,333,131 NEW ORDINARY SHARES OF RM0.05 EACH IN BIOALPHA ("BIOALPHA SHARE(S)") ("RIGHTS SHARE(S)") TOGETHER WITH 133,333,131 FREE NEW DETACHABLE WARRANTS ("WARRANTS") AT AN ISSUE PRICE OF RM0.20 ON THE BASIS OF 1 RIGHTS SHARE FOR EVERY 5 BIOALPHA SHARES HELD TOGETHER WITH 1 WARRANT FOR EVERY 1 RIGHTS SHARE SUBSCRIBED ("RIGHTS ISSUE WITH WARRANTS") | Unless otherwise defined, the terms used in this announcement shall have the same meaning as those defined in the announcement dated 7 September 2016.

We refer to the announcements dated 7 September 2016, 19 September 2016, 13 October 2016, 15 November 2016, 18 November 2016, 23 November 2016 and 24 November 2016 as well as the Abridged Prospectus in relation to the Rights Issue with Warrants dated 8 December 2016.

On behalf of Board of Directors of Bioalpha, Hong Leong Investment Bank Berhad wishes to announce that at the close of acceptance, excess application and payment for the Rights Issue with Warrants as at 5.00 p.m. on 27 December 2016 (“Closing Date”), the total valid acceptances and excess applications received for the Rights Issue with Warrants was 162,760,685 Rights Shares together with 162,760,685 Warrants. This represents a subscription rate of 122.07% of the total number of 133,333,131 Rights Shares together with 133,333,131 Warrants available for subscription under the Rights Issue with Warrants.

The details of the valid acceptances and excess applications received as at the Closing Date are as follows:

| No. of Rights Shares | % of total issue |

|

|

| Total valid acceptances | 119,468,609 | 89.60 | Total valid excess applications | 43,292,076 | 32.47 | Total valid acceptances and excess applications | 162,760,685 | 122.07 |

|

|

| Total Rights Shares available for subscription | 133,333,131 | 100.00 |

The Rights Shares and Warrants are expected to be listed on the Main Market of Bursa Securities on 10 January 2017.

This announcement is dated 4 January 2017. |

|

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 10-1-2017 03:52 AM

|

显示全部楼层

Instrument Category | Securities of PLC | Instrument Type | Warrants | Description | Issuance of free detachable warrants ("Warrants") pursuant to the renounceable rights issue of 133,333,131 new ordinary shares of RM0.05 each in Bioalpha ("Bioalpha Shares") ("Rights Shares") at an issue price of RM0.20 per Rights Share on the basis of 1 Rights Share for every 5 existing Bioalpha Shares held at 5.00 p.m. on 8 December 2016, together with 133,333,131 Warrants on the basis of 1 Warrant for every 1 Rights Share subscribed. |

Listing Date | 10 Jan 2017 | Issue Date | 06 Jan 2017 | Issue/ Ask Price | Not Applicable | Issue Size Indicator | Unit | Issue Size in Unit | 133,333,131 | Maturity | Mandatory | Maturity Date | 05 Jan 2022 | Revised Maturity Date |

| | Name of Guarantor | Not Applicable | Name of Trustee | Not Applicable | Coupon/Profit/Interest/Payment Rate | Not Applicable | Coupon/Profit/Interest/Payment Frequency | Not Applicable | Redemption | Not Applicable | Exercise/Conversion Period | 5.00 Year(s) | Revised Exercise/Conversion Period | Not Applicable | Exercise/Strike/Conversion Price | Malaysian Ringgit (MYR) 0.2200 | Revised Exercise/Strike/Conversion Price | Not Applicable | Exercise/Conversion Ratio | 1:1 | Revised Exercise/Conversion Ratio | Not Applicable | Mode of satisfaction of Exercise/ Conversion price | Cash | Settlement Type/ Convertible into | Physical (Shares) |

|

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 12-1-2017 05:36 AM

|

显示全部楼层

Name | MR HON TIAN KOK @ WILLIAM | Nationality/Country of incorporation | Malaysia | Descriptions (Class & nominal value) | Ordinary Shares of RM0.05 each | Name & address of registered holder | Hon Tian Kok @ WilliamNo 52A, Jalan 8/35ATaman Seri Bangi, Seksyen 843650 Bandar Baru BangiSelangor Darul Ehsan |

Details of changesCurrency: Malaysian Ringgit (MYR) | Type of transaction | Description of Others | Date of change | No of securities

| Price Transacted ($$)

| | Acquired | | 10 Nov 2016 | 218,500

| 0.240

| | Others | Rights Issue | 06 Jan 2017 | 25,119,467

| 0.200

|

Circumstances by reason of which change has occurred | Acquisition of Shares & Rights Issue with free detachable Warrants | Nature of interest | Direct | Direct (units) | 153,716,807 | Direct (%) | 19.21 | Indirect/deemed interest (units) | 0 | Indirect/deemed interest (%) | 0 | Total no of securities after change | 153,716,807 | Date of notice | 11 Jan 2017 |

|

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 14-1-2017 03:47 AM

|

显示全部楼层

Name | PERBADANAN NASIONAL BERHAD | Address | Level 16, Menara PNS Tower 7,

Avenue 7, Bangsar South City,

No. 8, Jalan Kerinchi

Kuala Lumpur

59200 Wilayah Persekutuan

Malaysia. | Company No. | 9157-K | Nationality/Country of incorporation | Malaysia | Descriptions (Class & nominal value) | Ordinary Shares of RM0.05 each | Name & address of registered holder | Perbadanan Nasional BerhadLevel 16, Menara PNS Tower 7, Avenue 7, Bangsar South City,No. 8, Jalan Kerinchi,59200 Kuala Lumpur |

Details of changesCurrency: Malaysian Ringgit (MYR) | Type of transaction | Description of Others | Date of change | No of securities

| Price Transacted ($$)

| | Others | Rights Issue | 06 Jan 2017 | 13,751,101

| 0.200

|

Circumstances by reason of which change has occurred | Pursuant to Rights Issue with free detachable Warrants | Nature of interest | Direct | Direct (units) | 82,505,606 | Direct (%) | 10.31 | Indirect/deemed interest (units) | 0 | Indirect/deemed interest (%) | 0 | Total no of securities after change | 82,506,606 | Date of notice | 13 Jan 2017 |

|

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 19-1-2017 04:13 AM

|

显示全部楼层

Name | MR HON TIAN KOK @ WILLIAM | Nationality/Country of incorporation | Malaysia | Descriptions (Class & nominal value) | Ordinary Shares of RM0.05 each | Name & address of registered holder | Hon Tian Kok @ WilliamNo 52A, Jalan 8/35ATaman Seri Bangi, Seksyen 843650 Bandar Baru BangiSelangor Darul Ehsan |

Details of changesCurrency: Malaysian Ringgit (MYR) | Type of transaction | Description of Others | Date of change | No of securities

| Price Transacted ($$)

| | Disposed | | 12 Jan 2017 | 6,301,500

| 0.225

| | Disposed | | 12 Jan 2017 | 8,096,600

| 0.224

|

Circumstances by reason of which change has occurred | Disposal of Shares | Nature of interest | Direct | Direct (units) | 132,616,807 | Direct (%) | 16.58 | Indirect/deemed interest (units) | 0 | Indirect/deemed interest (%) | 0 | Total no of securities after change | 132,616,807 | Date of notice | 17 Jan 2017 |

|

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 1-2-2017 04:40 AM

|

显示全部楼层

Name | MR HON TIAN KOK@WILLIAM | Nationality/Country of incorporation | Malaysia | Descriptions (Class & nominal value) | Ordinary Shares of RM0.05 each | Name & address of registered holder | Hon Tian Kok @ WilliamNo 52A, Jalan 8/35ATaman Seri Bangi, Seksyen 843650 Bandar Baru BangiSelangor Darul Ehsan |

Details of changesCurrency: Malaysian Ringgit (MYR) | Type of transaction | Description of Others | Date of change | No of securities

| Price Transacted ($$)

| | Disposed | | 31 Jan 2017 | 9,000,000

| 0.220

|

Circumstances by reason of which change has occurred | Disposal of Shares via open market transaction | Nature of interest | Direct | Direct (units) | 123,616,807 | Direct (%) | 15.45 | Indirect/deemed interest (units) | 0 | Indirect/deemed interest (%) | 0 | Total no of securities after change | 123,616,807 | Date of notice | 31 Jan 2017 |

|

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 20-2-2017 01:29 AM

|

显示全部楼层

科鼎控股值得投资?

科鼎控股小股东问:

创业板上市公司——科鼎控股(BIOHLDG,0179,创业板消费品组)

(一)这家公司是否还值得投资,

(二)公司是否有问题?

(三)公司盈利不断上升,股价却一直在跌,这是什么原因?

(四)是否有派息政策?我买进了这家公司后,股价一直下跌,红股后公司又马上建议附加股。现在终于等到附加股及凭单上市了,亏损也减少了,不过,想请问这家公司是否还值得持有?

(五)有没有目标价?

答:科鼎控股是否值得投资/或值得持有,没有证券行或分析员给予评估及建议。所以,也没有目标价建议。不过,以下的一些资料供估值参考。

该公司的核心业务为保健品制造与销售,业务分布至印尼、中国及中东。在大马亦有多家药剂店。值得注意一点,即是该公司的3大股东中,除了其最大单一股东-韩丁国持有19.21%股权,也包括国库控股及国民投资公司,排在第二及第三位,分别持股16.08%及10.31%。

关注发展潜能

上述两家投资公司通常都较为专业与严谨,特别是关注所投资公司的素质及条件与发展潜能,也是考虑是否值得持有的个中因素。

探探该公司最新业绩表现,截至2016年9月30日为止第三季,该公司净利为278万2000令吉(每股净利0.54仙),前期净利为255万2000令吉(每股净利为0.55仙)。营业额则增加至1208万8000令吉,前期为853万6000令吉。

首9个月净利则为430万令吉(每股净利为0.85仙),前期净利为296万3000令吉(每股净利为0.70仙)。营业额为3096万2000令吉,前期为2001万5000令吉。

财务情况方面,截至2016年9月30日为止,该公司总资产为1亿零802万6000令吉,包括现金与银行余款为1129万8000令吉。

其总负债则为1481万1000令吉。每股资产值为18.24仙。

该公司的总股本为7亿9999万8000股。

截至2017年1月24日为止,其收市价为21仙,这使该公司的市值为1亿6799万9000令吉。

这里稍为总结该公司对2016年12月31日为止财政年的业务展望,该公司乐观看待2016财政年的业绩表现;这包括整合其Constant药剂店,并计划将药剂业务通过特许专营权方式扩大分店数目,这不仅不会对公司资产负债表造成负担,同时,也可控制管理及成长方向。

该公司将在印尼设立制造厂以加速成长潜能。同时公司的药剂产品在中国市场受到欢迎,主要是积极进行促销及行销所致。

该公司也开始在龙运巴西拉惹进行第二阶段的清理土地活动,它涉及879.5英亩,以便种植市场受欢迎的药草。

(二)该公司是否有什么问题,则不得而知。

(三)该公司盈利上扬、惟股价却下跌,这可能是它刚完成红股、附加股及凭单计划,除权后股价相应调整回跌(盈利被冲淡),或是公司股本及流通量增加,从而仰制股价上升的个中主因。

(四)派息政策方面,相信该公司并没有固定的派息政策。它在2014财政年派发每股0.13仙股息、2015财政年则每股0.1仙股息、以及2016年首9个月里没有派发任何股息。

文章来源:

星洲日报‧投资致富‧投资问诊‧文:李文龙‧2017.02.19 |

|

|

|

|

|

|

|

|

|

|

|

发表于 3-3-2017 04:45 PM

|

显示全部楼层

发表于 3-3-2017 04:45 PM

|

显示全部楼层

本帖最后由 icy97 于 4-3-2017 02:38 AM 编辑

BIOHLDG (0179) 科鼎控股 - 收购了Constant药剂店,全年营业额提升60%。

Author: WeShare WeTrade | Publish date: Thu, 2 Mar 2017, 08:33 PM

https://klse.i3investor.com/blogs/wesharenwetrade/117435.jsp

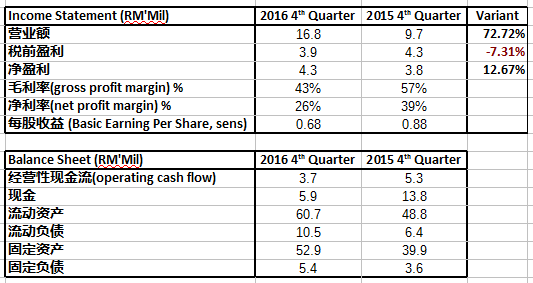

BIOHLDG在2016年末季记载着RM16.8Mil的营业额,与同期相比多了RM7Mil,进步多达72%!虽然业绩有起色,但税前盈利却不见比同期好,原因是开销(Administration Expenses)部分起了RM2.2Mil。公司有提到这开销提高是因为公司有新招聘在R&D(Research & Development)和连锁经营部门。而且公司近期也下重本在广告与促销活动来重新推广Constant药剂店。不过,税务回扣让净利超越去年同期。

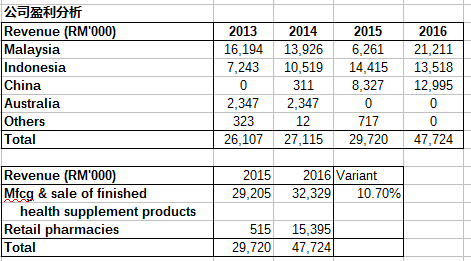

公司盈利分析

全年营业额RM47.7Mil提高了60%,净盈利也进步了27%。

净利率方面,就像预期所说的那样,会较上财年低。原因是公司加进了Retail Pharmacies的营业额,赚幅相比Manufacturing & Sales业务来得低,所以综合起来拉低了净利率。

但整体来说还是不错的(毛利率在41%),而且多了药剂店(Retail Pharmacies)将有助于公司推广自家产品(Apotec和NuShine)。

Manufacturing and Sale业务提升了RM3.1Mil或10.7%,主要原因是出口至中国的产品提高了56%,抵消了印尼市场业绩放缓的影响(下滑了6%)。

Retail Pharmacies方面就有着明显的进步,由于公司收购了14间药剂店“Constant”,业绩提升了RM14.88Mil。 2017年发展计划 1. 印尼市场 目标是在2017和2018年个推出6种新产品以提高民众需求。新生产线位于金宝将负责将产品提供于印尼市场。而且在印尼的生产配备将缩短新产品供应的时间,以便让新产品更快速在市场亮相。 2. 中国市场 公司正积极地在中国贸易展览会办营销活动,而且得到了有效的业绩成长。公司也开始选择在中国一些比较多穆斯林居住的地区来推广产品。

3. 本地市场 预计在2017和2018年推出5种新产品。好处是新产品一推出,各大Constant和其他药剂店将有助于推广。而且公司还会努力翻新自家品牌,通过连锁药剂店来推广。下个新市场将会在吉兰丹,柔佛和吉打。而在今年3月,又有一间药剂店位于Bangi将开张营业。 回顾投资亮点/企业估值 1. 行业 在保健品的行业里,一直都是稳定的成长。我们可以因为经济不景而延迟买房子的时间,但不能拖延保健自己的身子。现时代,人们会多加留意慢性疾病,快速城市化,老龄化社会的问题等。这也导致保健品需求量一直可以保持正面成长。

2. 产品

公司可以收割自己的农业务做草药保健品,而且每年都会推出新产品,相信公司业务还有很大的市场发展空间。

3. 公司基本面

公司业绩提升,负债少,Current Ratio在5.7,基本面良好。BIOHLDG在近期发行附加股和配送凭单,得到热烈回响,认购率超额至22.1%或1.22倍。

而公司所发售133Mil的新股,成功筹集26.7Mil的资金来扩展业务,推出新产品。相信以公司积极的开阔市场,今年里将会有好的业绩回报。持股需要耐心,小编依然认为BIOHLDG会是潜力股之一。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 4-3-2017 01:25 PM

|

显示全部楼层

本帖最后由 icy97 于 5-3-2017 12:34 AM 编辑

BIOALPHA On Going Study Case #2 Q416

Author: leonnoel | Publish date: Fri, 3 Mar 2017, 01:54 PM

https://klse.i3investor.com/blogs/bioalpha/117505.jsp

Reading Q416 report the day it was released, I got to a weird conclusion that I am not sure where the price would go in a short term bases. In general nothing went wrong, the company is going in the right direction with a heathy result, at the same time nothing went incredibly right.

Again, I am merely a new comer in investment, certain of many wrongs, couples of questions. Sober comments are welcome.

-----------------------------------------

things that stood out in the report

Revenue look impressive from Q415 9.7m to Q416 16.76m (73% increase), but notice that this include 4m of pharmacies revenue. The actual comparison (since Q42015 does not has pharmacies revenue) will be from 9.7m to 12.7m (31% increase). The annual 2015-2016 comparison exclyuding retail pharmacies is merely a 10.6% growth (29.2m to 32.3m). It doesn't mean retail pharmacies area doesn't matter, but I think is only fair to compare the same factors, then only consider new factors.

A 10.6% growth in core business is not a great number for Biohldg, which I view as a developing stock type. Yet it is acceptable as its plantation, upgrade and expansion plans have just began in late 2016. These plans blossom around Q417~H218, talk in detail below.

Unfortunately the cost of sales is not segmented, so there is no way to tell whether the gross profit margin in core business dropped or not. The drop in GPM from Q415 57% (5.5/9.7m) to Q416 43% (7.3m/16.8m) is said to be because of retailing's low margin and I have no opposition to this explanation. One rather important thing that should happen in the future is the cost of sales should be decreasing mainly becuase of the reduced cost of raw materials supply since Bio started to plant its own herbs.

The administration expenses increased from 4m to 6.2m (55%) due to recruitment in R&D, franchise department, marketing for the pharmacy company(Constant). While I have no opposition to this explanation, keep in mind that the marketing/rebranding of Constant would eventually goes away but the increased cost for new recruits is here to stay.

Profit before tax decreased from Q415 4.3m to Q416 3.9m, keep in mind the increase in administration expenses of 2.2m. Bio's net profit barely increased from Q415 3.8m to Q416 4.3m, with the help of tax return. I have a neutral-positive view on this one, credits to Bio on keeping profit level while spending to expand.

Cash flow decreased from Q3 15m to 5m, I do not understand the sudden jump in trade receivables, but the historical impairment is quick low and it should be fine. The other is an increase in investing in property, plant and equipment. I am not clear about the details of this spending of cash but I could agree with themanagement to spend it, since they would be receiving 26.7m in January 2017. They should began their expansion as soon as possible by spending their cash flow, knowing that there would be 26.7m coming in.

The revenue increase mainly came from the increase in China revenue (Q316 3.6m to Q416 6.8m), which is great/amazing. But the sales revenue in Malaysia is rather mediocre when pharmacies sales is removed (pharmacies sales also remained mediocre)

The eps is .679 calculated at 666.666m shares (Q415 is .88). Again from my previous article, the concern I have with Bio is the continuos dilution from shares issuing. We must understand that, Q117 would have 133.333m more shares from right issue, 29m share issuance scheme option(more to come as they are allow to issue up to 279.999m) and 133.333m warrant. Of course, the SIS option and warrant should not be taken as face number for dilution. An assumption of 5% execution rate would dilute shares by 21%(141.45/666.666m), using 2016 profit (8.27m) we would get an annual eps of 1.02. Which made the stock quite expensive even in my collected price .21(PE of 20.6), not to mention at its current price .25 (PE 24.5). Keep in mind the shares will be further diluted in the future until the toal shares reached to 1213.33m. This simply mean Bio's future earning has to catch up to, conservatively at least 30% grow for this year (with the consideration that this year warrant and option execution within 5%). Another concern would be the ROE (7.48%, is already not a great number), the 26.7m from right issue funding would bring up the equity by 27% (26.7/97.74m), further diluting its ROE, yet I believe with so many plans running Bio would know where to spend these funding to at least math previous ROE in the future.

The grow aspects of this stock remained the same, products expansion and plantation mentioned in my first article. Again, my expectation of explosive grow for this stock in term of earning will be the period of Q417~2h18. Yes Bio have purchased some new machineries to produce better products, but the 'ordering and put into use'/aka delay time is 6 to 12 months based on their right issue explanation special report. Yes Bio is starting to plant in Pasir Raja for the remaining 880 acre of land, but remember when Bio planted 124 acre in Q216, only 10% of those herbs are harvestable in Q416. Considering the same case, if Bio is able to plant 30% of 880 acre (264 acre) in Q117, only 10% (26.4acre) of herbs would be harvestable in Q317. The first new products launch 1H17, 5 in Malaysia, 3 in Indonesia, 3 in China, really I would expect the responses/effect came in 2H17. All these things above begin its effect from 2H17 and slow down towards 2H18.

Summary:

Good revenue from China. Good spending of cash flow. EPS is still going to get diluted in the future. Nothing much changes from my previous article view, a great potantial developing company with heathy grow in this Q416 report. The expectation of explosive grow of earning would be in the period of Q417~2H18.

|

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 7-3-2017 04:42 AM

|

显示全部楼层

SUMMARY OF KEY FINANCIAL INFORMATION

31 Dec 2016 |

| | INDIVIDUAL PERIOD | CUMULATIVE PERIOD | CURRENT YEAR QUARTER | PRECEDING YEAR

CORRESPONDING

QUARTER | CURRENT YEAR TO DATE | PRECEDING YEAR

CORRESPONDING

PERIOD | 31 Dec 2016 | 31 Dec 2015 | 31 Dec 2016 | 31 Dec 2015 | $$'000 | $$'000 | $$'000 | $$'000 |

| 1 | Revenue | 16,762 | 9,705 | 47,724 | 29,720 | | 2 | Profit/(loss) before tax | 3,943 | 4,254 | 8,074 | 7,302 | | 3 | Profit/(loss) for the period | 4,304 | 3,820 | 8,267 | 6,458 | | 4 | Profit/(loss) attributable to ordinary equity holders of the parent | 4,529 | 3,833 | 8,829 | 6,796 | | 5 | Basic earnings/(loss) per share (Subunit) | 0.68 | 0.88 | 1.32 | 1.55 | | 6 | Proposed/Declared dividend per share (Subunit) | 0.00 | 0.00 | 0.00 | 0.00 |

|

| AS AT END OF CURRENT QUARTER | AS AT PRECEDING FINANCIAL YEAR END | 7

| Net assets per share attributable to ordinary equity holders of the parent ($$) | 0.1466 | 0.1798

|

|

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 7-4-2017 04:44 AM

|

显示全部楼层

扩网络.推产品.科鼎发展潜能看好

(吉隆坡5日讯)科鼎控股(BIOHLDG,0179,创业板消费品组)为大马合作社组织(ANGKASA)提供在线药剂服务,规模有望再扩展,同时计划为海外业务推出新产品,发展潜能受分析员看好。

上周,科鼎控股推出网上药剂店e-Constant,供联营伙伴马来西亚合作社组织专用,联昌研究表示,该公司可藉此特许经营业务,提升其制药及品牌销售,但因新推出,目前未能预测潜在盈利。

不过,该行认为,因该组织概括1万2000家合作社,会员多达800万名,加上该公司有意将e-Constant再推销至规模更大的大马皇家警察、马电讯(TM,4863,主板贸服组)员工合作社(Kotamas)及国油员工合作社(Kopetro),估计网上药剂店具有强大的发展潜能。

海外业务方面,该行指出,印尼廖内省的新厂房可缩短公司产品注册待批时间,过去需2至3年的等候期,如今只需3至6个月。至于中国,除了目前的5种产品,科鼎也有意在今年上半年内推出3种,下半年再推出2种,并销售至穆斯林密集的中国地区,尤其西北部。

该行预测,在新产品及多达一亿人口的中国穆斯林市场提振下,海外业务可在2017年录得亮眼成绩,回顾2016财政年,印尼及中国业务分别占该公司营收的41%及40%。

综合以上,联昌研究维持该公司的盈利预测,2017财政年净利料可按年涨近70%,至1388万令吉;2018年则预测为1750万令吉,且因2018财政年可达13.3倍的本益比。

该行维持科鼎控股的“加码”评级及37仙的目标价。

文章来源:

星洲日报‧财经‧报道:陈学颖‧2017.04.05

|

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 19-4-2017 07:16 AM

|

显示全部楼层

Name | MR HON TIAN KOK @ WILLIAM | Nationality/Country of incorporation | Malaysia | Descriptions (Class & nominal value) | Ordinary Shares | Name & address of registered holder | Hon Tian Kok @ WilliamNo. 31, Jln SL5/1, Bandar Sungai Long, 43000 Kajang, Selangor Darul Ehsan.WH Capital Sdn BhdNo. 5-4-1, Jalan 3/50,Diamond Square,Off Jalan Gombak,53000 Kuala Lumpur. |

Details of changesCurrency: Malaysian Ringgit (MYR) | Type of transaction | Description of Others | Date of change | No of securities

| Price Transacted ($$)

| | Disposed | | 17 Apr 2017 | 1,000,000

| 0.258

| | Disposed | | 18 Apr 2017 | 7,000,000

| 0.255

| | Acquired | | 18 Apr 2017 | 18,751,502

| 0.235

|

Circumstances by reason of which change has occurred | 1. Disposal of shares via open market transaction2. Acquired of shares via off market transaction | Nature of interest | Direct Interest and Indirect Interest | Direct (units) | 109,616,807 | Direct (%) | 13.7 | Indirect/deemed interest (units) | 18,751,502 | Indirect/deemed interest (%) | 2.344 | Total no of securities after change | 128,368,309 | Date of notice | 18 Apr 2017 |

|

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 27-4-2017 04:37 AM

|

显示全部楼层

Date of change | 21 Apr 2017 | Name | MISS GOH SIOW CHENG | Age | 35 | Gender | Female | Nationality | Malaysia | Type of change | Others | Designation | Chief Financial Officer | Description | Promoted from Finance Controller to Group Chief Financial Officer | Qualifications | Bachelor of Business (Accounting & Finance) from University of Technology Sydney, Australia in 2003 and become a member of CPA Australia since 2007 | Working experience and occupation | Goh Siow Cheng began her career with Grant Thornton, Malaysia as an Audit Associate in 2004 and was with the firm until 2010, where her last position was Senior Manager. She joined Ernst & Young, Singapore as an Audit Manager in 2010 and subsequently left to join Wasco Energy group of companies as Finance Manager in 2012. Throughout her career, she has served in various private or public limited companies and industries including manufacturing, trading, property development, information technology and plantation. She was Finance Controller of the Company since 2014 and was promoted to Group Chief Financial Officer on 21 April 2017. | Family relationship with any director and/or major shareholder of the listed issuer | Nil | Any conflict of interests that he/she has with the listed issuer | Nil | Details of any interest in the securities of the listed issuer or its subsidiaries | Ordinary Shares - NilWarrants - 34 Warrants |

|

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 28-4-2017 03:24 AM

|

显示全部楼层

Name | PERBADANAN NASIONAL BERHAD | Address | Level 16, Menara PNS Tower 7

Avenue 7, Bangsar South City

No. 8 Jalan Kerinchi

Kuala Lumpur

59200 Wilayah Persekutuan

Malaysia. | Company No. | 9157-K | Nationality/Country of incorporation | Malaysia | Descriptions (Class & nominal value) | Ordinary shares | Name & address of registered holder | Perbadanan Nasional Berhad Level 16 Menara PNS Tower 7Avenue 7, Bangsar South CityNo. 8 Jalan Kerinchi59200 Kuala Lumpur |

Details of changesCurrency: Malaysian Ringgit (MYR) | Type of transaction | Description of Others | Date of change | No of securities

| Price Transacted ($$)

| | Disposed | | 18 Apr 2017 | 18,751,502

| 0.235

|

Circumstances by reason of which change has occurred | Disposal of shares via off market transaction | Nature of interest | Direct Interest | Direct (units) | 63,755,104 | Direct (%) | 7.96 | Indirect/deemed interest (units) | 0 | Indirect/deemed interest (%) | 0 | Total no of securities after change | 63,755,104 | Date of notice | 26 Apr 2017 |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 31-5-2017 05:18 PM

来自手机

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 20-6-2017 04:17 PM

|

显示全部楼层

科鼎为何不涨?

一直亏损的小股东问:

关于创业板上市公司——科鼎控股(BIOHLD,G0179,创业板消费品组)

1.刚出来的第一个季度业绩如何?

2.为何营业额上涨,但净利却是亏损?

3.新闻一直发布公司积极向上扩充和发展,但股价却迟迟不上涨,还一直下跌,公司有什么问题?

4.我已经持有了这家公司接近2年了,却一直亏损。是否继续持有,还是止损离场?

答:首季转亏195万

(一)截至2017年3月31日第一季,科鼎控股由盈转亏,即蒙受净亏损195万5000令吉(每股净亏损0.25仙),前期取得净利12万2000令吉(每股净利0.03仙)。

首季营业额增长24.89%,至863万1000令吉,前期为690万8000令吉。该公司每股资产值为15.73仙。

开销走高抵销营收增长

(二)该公司首季营业额增长24.89%,主要是旗下保健辅助品营业额增加156万令吉或47.85%,因受到出口成长推动,包括印尼市场增加77.58%,至258万令吉;出口至中国市场也增加53.13%,至147万令吉等推动。

该公司旗下的零售药剂业务,营业额微增4.38%,至381万令吉。同时盈利赚幅也走高至34.38%,较前期为31.33%。

虽然该公司首季营业额增长,不过却是由盈转亏,主要是行政开支走高,包括颁予员工的股票发行计划提供180万令吉的合理价费用。同时,该公司也为附加股计划提供55万令吉的一次过企业活动开支。

若没有包括上述的两项开支,该公司首季税前盈利则为30万令吉或净利26万令吉,比前期的12万2000令吉高出14万令吉或116.67%。

盈利不显著

股价涨不起

(三)虽然科鼎控股一直发表会积极向上的扩充和发展,股价却迟不上涨,反而一直下跌的问题,从该公司过去逾两年、或是9个季度的业绩表现记录显示,除了最新的首季出现亏损,其余8个季度都是有利可图,不过盈利都不显著。

同期间,该公司股本回酬率最高达4.64%、期间进行过私下配售计划、红股(3送1)及附加股计划,包括2017年1月10日完成5配1送1凭单的附加股计划,从而进一步冲稀盈利等情况,相信是其股价不起走跌个中原因。

上述的一点资料,可能是使其股价下跌(相应调整)原因,除此以外,是否还有其他问题,则不得而知。

扩海内外业务

需时见成果

(四)科鼎控股在宣布最新业绩时,表示在今年1月10落实的附加股计划,为公司筹得2670万令吉的资金,主要充当推动未来两年的成长计划,特别是扩充大马、中国及印尼的市场及提升农业业务的营运,其成果如何则拭目以待。

不过,该公司对截至2017年12月31日财政年的业绩表现持乐观态度。有鉴于此,是否要继续持有、还是止损离场,没有证券行给予剖析及推荐。

文章来源:

星洲日报‧投资致富‧投资问诊‧文:李文龙‧2017.06.18 |

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 10-8-2017 04:51 AM

|

显示全部楼层

Name | PERBADANAN NASIONAL BERHAD | Address | Level 16, Menara PNS Tower 7

Avenue 7, Bangsar South City

No. 8 Jalan Kerinchi

Kuala Lumpur

59200 Wilayah Persekutuan

Malaysia. | Company No. | 9157-K | Nationality/Country of incorporation | Malaysia | Descriptions (Class) | Ordinary shares |

Details of changesNo | Date of change | No of securities | Type of Transaction | Nature of Interest | | 1 | 07 Aug 2017 | 9,946,600 | Acquired | Direct Interest | Name of registered holder | Perbadanan Nasional Berhad | Address of registered holder | Level 16, Menara PNS Tower 7, Avenue 7, Bangsar South City No. 8 Jalan Kerinchi, 59200 Kuala Lumpur | Description of "Others" Type of Transaction | |

Circumstances by reason of which change has occurred | Acquisition of shares via open market | Nature of interest | Direct Interest | Direct (units) | 73,701,704 | Direct (%) | 9.139 | Indirect/deemed interest (units) | 0 | Indirect/deemed interest (%) | 0 | Total no of securities after change | 73,701,704 | Date of notice | 08 Aug 2017 | Date notice received by Listed Issuer | 09 Aug 2017 |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 19-8-2017 04:20 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 24-8-2017 06:05 AM

|

显示全部楼层

SUMMARY OF KEY FINANCIAL INFORMATION

30 Jun 2017 |

| | INDIVIDUAL PERIOD | CUMULATIVE PERIOD | CURRENT YEAR QUARTER | PRECEDING YEAR

CORRESPONDING

QUARTER | CURRENT YEAR TO DATE | PRECEDING YEAR

CORRESPONDING

PERIOD | 30 Jun 2017 | 30 Jun 2016 | 30 Jun 2017 | 30 Jun 2016 | $$'000 | $$'000 | $$'000 | $$'000 |

| 1 | Revenue | 13,157 | 11,966 | 21,788 | 18,874 | | 2 | Profit/(loss) before tax | 2,506 | 1,379 | 452 | 1,413 | | 3 | Profit/(loss) for the period | 2,456 | 1,284 | 372 | 1,295 | | 4 | Profit/(loss) attributable to ordinary equity holders of the parent | 2,469 | 1,395 | 514 | 1,518 | | 5 | Basic earnings/(loss) per share (Subunit) | 0.31 | 0.28 | 0.07 | 0.31 | | 6 | Proposed/Declared dividend per share (Subunit) | 0.00 | 0.00 | 0.00 | 0.00 |

|

| AS AT END OF CURRENT QUARTER | AS AT PRECEDING FINANCIAL YEAR END | 7

| Net assets per share attributable to ordinary equity holders of the parent ($$) | 0.1581 | 0.1793 |

|

|

|

|

|

|

|

|

|

|

| |

本周最热论坛帖子 本周最热论坛帖子

|

1946

1946  236

236